The above chart illustrates the history of Canada’s federal debt (not including provincial and municipal debts: debtclock.ca). Obviously something went terribly wrong after 1974.

Over a 108 year period (1867-1974) the accumulated debt shows as nearly a flat line growing to only $21.6 billion. But around 1974, the debt began to grow exponentially and, over a mere 39 years, it reached over $600 billion in 2013.

What happened in Canada in 1974 ?

See: chriswick.ca/who-changed-the-bank-of-canadas-policies-in-1974-and-why. Also, in 1974 the Basel Committee was established by the central bank Governors of the group of ten countries of the member central banks of the Bank for International Settlements (BIS) ccc4mr.wordpress.com/bis/ which included Canada. A key objective of the Committee was and is to maintain “monetary and financial stability.”To achieve that goal, the Committee discouraged borrowing from a nation’s own central bank interest-free and encouraged borrowing from private creditors, all in the name of “maintaining the stability of the currency.”

The presumption was that borrowing from a central bank with the power to create money on its books would inflate the money supply and prices. Borrowing from private creditors, on the other hand, was considered not to be inflationary, since it involved the recycling of pre-existing money. What the bankers did not reveal, although they had long known it themselves, was that private banks create the money they lend just as public banks do — out of thin air. The difference is simply that a publicly-owned national central bank (Bank of Canada) returns the interest to the government and the People of the country, while a privately-owned bank siphons the principal plus interest into its capital account, to be re-loaned at further interest, progressively drawing money out of the productive economy.1

Paul Hellyer,2 also notes that lobbying by the banks and adoption of monetarism — the idea that “markets know best” and should be “without regulation,” and that public services should be privatized — took hold.

Since 1974, the Bank of Canada has not been acting in the best interest of its shareholders: the People of Canada.

To understand how ridiculous the present situation is, consider the 1993 Auditor General of Canada report (Section 5.41)3 which states:

The cost of borrowing is the third area that affects the annual deficit. In 1991-92, the interest on the debt was $41 billion. This cost of borrowing and its compounding effect have a significant impact on Canada’s annual deficits. From Confederation up to 1991-92, the federal government accumulated a net debt of $423 billion. Of this, $37 billion represents the accumulated shortfall in meeting the cost of government programs since Confederation. The remainder, $386 billion, represents the amount the government has borrowed to service the debt created by previous annual shortfalls.

Of the accumulated debt of $423 billion, the government really needed to borrow only $37 billion—accumulated over 127 years—to cover its shortfalls on real spending for goods and services. The rest of that accumulated debt was monies borrowed to service the debt, essentially a payment of interest on interest to the private sector when the government could have created the money to cover the shortfall at what amounts to be no interest.

According to Paul Hellyer, from 1974–1975 to 2010, Canadian taxpayers have paid over one Trillion, 100 billion dollars ($1,100,000,000,000) in interest alone on the federal debt to private lenders.4In 2011, alone, Canadian taxpayers paid the private banks an estimated $37.7 billion to service the federal debt—over $103 million each and every day of the year!5 These are tax dollars that, ceteris paribus, could have gone towards infrastructure, health care, education, and other social needs, if the Government of Canada used it’s own national, public Bank of Canada to create the money to cover its shortfall. Ultimately, the government could pay off the federal debt through the same means.

And consider this: from the time of confederation until 1974, Canada fought two world wars, went through a major depression, constructed major infrastructures such as the St. Lawrence Seaway, Trans-Canada Highway, International airports, Canadian National Railway, and brought in social welfare programs such as Family Allowance, Old Age Security pensions, Canada Pension Plan, Universal Health Care and wound up with a total accumulated debt of only $21.6 billion. Today (as of 2015) Canada’s total debt (federal, provincial and municipal) is already over one TRILLION dollars (and growing); total compounded interest on the debt paid to private banks since 1974 was also already over one TRILLION dollars, and the government is continually cutting services in order to be able to keep paying off the rapidly growing debt and the compounded interest on it, while our infrastructure is not being maintained. Meanwhile, the private banks keep increasing their already obscene profits. This unconstitutional “subsidy” to the private banks must end.

“There must be a discussion, to show how experience is to be interpreted. Wrong opinions and practices gradually yield to fact and argument: but facts and arguments, to produce any effect on the mind, must be brought before it.”

– John Stuart Mill, 1806-1873

With the onset of the federal election, the following information should be known by all candidates and taxpayers alike.

In 2009, Canadians paid $160 million per day, $58,7 billion for the year, in interest on federal, provincial and municipal debt. These costs lead to higher taxes and fees, cutbacks in public services and deterioration of public infrastructure. Much of this debt-service cost could be eliminated by greater use of the Bank of Canada to finance government investments.

Because the bank is wholly owned by Canada, all profits on its lending activity go to the government. This means that borrowing from the bank by the government is almost costless.

For years, the government borrowed from the Bank of Canada and, during that time, contrary to t he fears raised by opponents of the idea, run-away inflation never occurred.

By 1975, federal net debt amounted to $19 billion. Then, the government began to shift more of its borrowing from the Bank of Canada to the private sector – especially chartered banks, insurance companies and other large corporations.

By March 31, 2010, the net debt had ballooned to $583 billion and interestbearing debt had reached $763 billion.

The interest cost to taxpayers for the federal government’s debt is currently a $29 billion drain on federal revenues.

In addition, the use of the Bank of Canada to finance public debt would reduce the influence of large corporations on government policy decisions.

We should only vote for candidates who support the use of the Bank of Canada for the purposes described above.

A Good Stewardship of All Lifeis the core value of the United People Foundation(UPF) and it’s based on the Universal Declaration on Human Rights. We see a world of abundance and peace. Waste, injustice, poison, war and poverty belong in the museum.

Right now, the UPF focus is on the implementation of a simple, pure, efficient, just, transparent pro-life financial system.

A cooperative fairtrade pro-life bank in formation

BANK of Joy is a citizens initiative by professionals. We will introduce the fixed value currency URA, and as soon as we have more than 10,000 members we will apply for a banking license. We don’t use interest and because of this, we are the first real sustainable financial initiative in Europe. Interest is like a parasite. It causes shortages and crisis just like the current crisis. Instead of interest we do offer financial, ecological, emotional and social returns, on the basis of natural growth. We invest in local economies and sustainable projects for a healthy and just society. A bank of, for and by the people in which we will manage our money ourselves.

B of Joy and the URA will make irreversible transitions possible. This B of Joy project is exclusively of service to society. So we ask for support and collaboration from society itself.

In this way the products and services are most optimally tuned to the needs of the community. B of Joy is a citizens’ initiative of professionals. Feel free to take part in the execution and realization of our projects, products and services.

12-year old Victoria Grant explains why her country, Canada, and most of the world, has been being robbed and bankrupted:

Have you ever wondered why Canada is in debt? Have you ever wondered why the government forces Canadians to pay so many taxes? Have you ever wondered why the bankers from the largest private banks are becoming wealthier, and the rest of us are not? Have you ever wondered why the gross national debt is over $800 billion dollars? Or, why we are spending $160 million dollars a day on the interest of the national debt? That is $60 billion dollars a year! Have you ever wondered who receives the $60 billion dollars?

What I have discovered is the banks and the government have colluded to financially enslave the people of Canada.

I will share with you three important points of reference which will hopefully spark enough interest and concern for you to continue the research on your own and to engage your government to stop this criminal act against the people of Canada.

First, we will briefly examine the Bank of Canada;

Second, we will see how the banking system works today;

And lastly, I will offer a viable solution that we can petition our government to implement.

A very little known figure in Canadian history is Gerald Grattan McGeer. He was a lawyer, a Member of Parliament and Mayor of Vancouver. His contribution to Canada is probably one of the greatest in our history. He championed the creation of the National Bank of Canada whose sole purpose is to create and manage Canada’s money. It was formed on July 3rd, 1934 and owned by all Canadians.

Allow me to explain how our private banks and government work today: first the Canadian government borrows money from the Private Banks. They then lend the debt based money to Canada, with compounded interest. The government then continues to increase taxation of Canadians, year after year, in order to pay back the interest on the exponentially growing national debt. What results is inflation, less real money for Canadians to spend into our economy, and the real money being used to pad the pockets of the banks.

As well, the government gave the banks the ability to loan out money that doesn’t exist in the form of loans. When a bank actually gives you a mortgage, which literally means a death pledge, or a loan, the banks do not actually give you money. They click a key on a computer and generate the fake money out of thin air. They don’t actually have it in their bank vaults. Presently, the banks only have 4 billion dollars on reserve, but they have loaned out over 1.5 Trillion dollars.

To quote Graham Towers, Each and every time a bank makes a loan, a new bank credit is created, brand new money. Broadly speaking, all new money comes out of a bank in the form of loans. As loans are debt, then under the present system all money is debt.

What I find interesting is that even Jesus (in Matthew 21) drove out the money changers from the temple, because they were manipulating the currency to steal money from the people.

In an infamous interview Mr. McGeer asked Mr. Towers, Can you tell me why a government with power to create money should give that power away to a private monopoly, and then borrow that which parliament can create itself, back at interest, to the point of national bankruptcy?

In other words, if the Canadian government needs money, they can borrow it directly from the Bank of Canada. The people would then pay fair taxes to repay the Bank of Canada; this tax money would in turn get injected back into our economic infrastructure and the debt would be wiped out. Canadians would again prosper with real money as the foundation of our economic structure and not debt money.

Regarding, the debt money that is owed the private banks such as the Royal Bank, we would simply have the Bank of Canada print the money owing, hand it over to the private banks, and then clear the debt with the Bank of Canada. And yes, we have the power and lawful right to do so.

In conclusion, it has become painfully obvious, even for me, a 12 year old Canadian, that we are being defrauded and robbed by the banking system and a complicit government.

What will we do to stop this crime? What will we do to ensure that the next generation will live free and clear of the debt based economy that enslaves them to the bankers?

Margaret Mead said, and I hope that all of you remember this: “Never doubt that a small group of commited people can change the world. Indeed, it is the only thing that ever has.”

Thank you.

Out of the Mouths of Babes: Twelve-Year-Old Money Reformer Tops a Million Views

The youtube video of 12-year old Victoria Grant speaking at the Public Banking in America Conference has gone viral, topping a million views on various websites.

Monetary reform—the contention that governments, not banks, should create and lend a nation’s money—has rarely even made the news, so this is a first. Either the times they are a-changin’, or Victoria managed to frame the message in a way that was so simple and clear that even a child could understand it.

Basically, her message was that banks create money “out of thin air” and lend it to people and governments at interest. If governments borrowed from their own banks, they could keep the interest and save a lot of money for the taxpayers.

She said her own country of Canada actually did this, from 1939 to 1974. During that time, the government’s debt was low and sustainable, and it funded all sorts of remarkable things. Only when the government switched to borrowing privately did it acquire a crippling national debt.

Borrowing privately means selling bonds at market rates of interest (which in Canada quickly shot up to 22%), and the money for these bonds is ultimately created by private banks. For the latter point, Victoria quoted Graham Towers, head of the Bank of Canada for the first twenty years of its history. He said:

Each and every time a bank makes a loan, new bank credit is created — new deposits — brand new money. Broadly speaking, all new money comes out of a Bank in the form of loans. As loans are debts, then under the present system all money is debt.

Towers was asked, “Will you tell me why a government with power to create money, should give that power away to a private monopoly, and then borrow that which parliament can create itself, back at interest, to the point of national bankruptcy?” He replied, “If Parliament wants to change the form of operating the banking system, then certainly that is within the power of Parliament.”

In other words, said Victoria, “If the Canadian government needs money, they can borrow it directly from the Bank of Canada. The people would then pay fair taxes to repay the Bank of Canada. This tax money would in turn get injected back into the economic infrastructure and the debt would be wiped out. Canadians would again prosper with real money as the foundation of our economic structure and not debt money. Regarding the debt money owed to the private banks such as the Royal Bank, we would simply have the Bank of Canada print the money owing, hand it over to the private banks, and then clear the debt to the Bank of Canada.”

Problem solved; case closed.

But critics said, “Not so fast.” Victoria might be charming, but she was naïve.

One critic was William Watson, writing in the Canadian newspaper The National Post in an article titled “No, Victoria, There Is No Money Monster.” Interestingly, he did not deny Victoria’s contention that “When you take out a mortgage, the bank creates the money by clicking on a key and generating ‘fake money out of thin air.’” Watson acknowledged:

Well, yes, that’s true of any “fractional-reserve” banking system. Even before they were regulated, even before there was a Bank of Canada, banks understood they didn’t have to keep reserves equal to the total amount of money they’d lent out: They could count on most depositors most of the time not showing up to take out their money all at once. Which means, as any introduction to monetary economics will tell you, banks can indeed “create” money.

What he disputed was that the Canadian government’s monster debt was the result of paying high interest rates to banks. Rather, he said:

We have a big public debt because, starting in the early 1970s and continuing for three full decades, our governments spent more on all sorts of things, including interest, than they collected in taxes. . . . The problem was the idea, still widely popular, from the Greek parliament to the streets of Montreal, that governments needn’t pay their bills.

That contention is countered, however, by the Canadian government’s own Auditor General (the nation’s top accountant, who reviews the government’s books). In 1993, the Auditor General noted in his annual report:

The cost of borrowing and its compounding effect have a significant impact on Canada’s annual deficits. From Confederation up to 1991-92, the federal government accumulated a net debt of $423 billion. Of this, $37 billion represents the accumulated shortfall in meeting the cost of government programs since Confederation. The remainder, $386 billion, represents the amount the government has borrowed to service the debt created by previous annual shortfalls.

In other words, 91% of the debt consists of compounded interest charges. Subtract those and the government would have a debt of only C$37 billion, very low and sustainable, just as it was before 1974.

Mr. Watson’s final argument was that borrowing from the government’s own bank would be inflationary. He wrote:

Victoria’s solution is that instead of paying market rates the government should borrow directly from the Bank of Canada and pay only token rates of interest. Because the government owns the bank, the tax revenues it raises in order to pay that interest would then somehow be injected directly back into the economy. In other words, money literally printed to cover the government’s deficit would be put into circulation. But how is that not inflationary?

Let’s see. The government can borrow money that ultimately comes from private banks, which admittedly create it out of thin air, and soak the taxpayers for a whopping interest bill; or it can borrow from its own bank, which also creates the money out of thin air, and avoid the interest.

Even a 12-year old can see how this argument is going to come out.

Huffington Post —Victoria Grant, 12, Hits Lecture Circuit To Explain How Canadian Banking Is A Fraud:

Ellen Hodgson Brown, J.D., developed her research skills as an attorney practicing civil litigation in Los Angeles. She is the author of 12 books. In Web of Debt, she traces the history and evolution of the current private banking system. She shows how it has usurped the power to create money from the people themselves, and how we the people can get it back. Her over 300 blog articles are at EllenBrown.com. She is the inspiration and thought leader behind the Public Banking Institute, where she serves as Chairman and President. She has degrees from UC Berkeley and UCLA School of Law.

“It’s Our Money with Ellen Brown” provides a unique view behind the curtain of global finance and the monetary system by one of the top experts in the field:

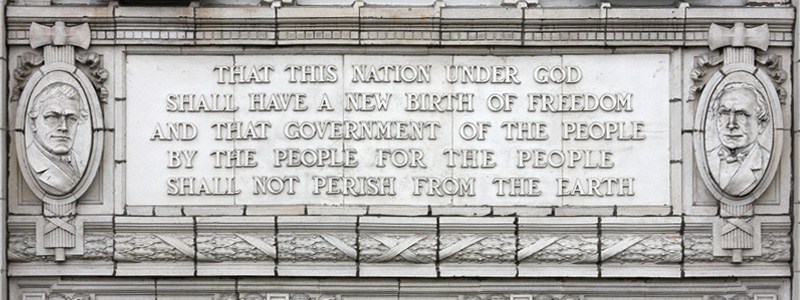

Government of the people, by the people, and for the people

According to a new study from Princeton University, American democracy no longer exists. Using data from over 1,800 policy initiatives from 1981 to 2002, researchers Martin Gilens and Benjamin Page concluded that rich, well-connected individuals on the political scene now steer the direction of the country, regardless of – or even against – the will of the majority of voters. America’s political system has transformed from a democracy into an oligarchy, where power is wielded by wealthy elites.

“Making the world safe for democracy” was President Woodrow Wilson’s rationale for World War I, and it has been used to justify American military intervention ever since. Can we justify sending troops into other countries to spread a political system we cannot maintain at home?

The Magna Carta, considered the first Bill of Rights in the Western world, established the rights of nobles as against the king. But the doctrine that “all men are created equal” – that all people have “certain inalienable rights,” including “life, liberty and the pursuit of happiness” – is an American original. And those rights, supposedly insured by the Bill of Rights, have the right to vote at their core. We have the right to vote but the voters’ collective will no longer prevails.

In Greece, the left-wing populist Syriza Party came out of nowhere to take the presidential election by storm; and in Spain, the populist Podemos Party appears poised to do the same. But for over a century, no third-party candidate has had any chance of winning a US presidential election. We have a two-party winner-take-all system, in which our choice is between two candidates, both of whom necessarily cater to big money. It takes big money just to put on the mass media campaigns required to win an election involving 240 million people of voting age.

In state and local elections, third party candidates have sometimes won. In a modest-sized city, candidates can actually influence the vote by going door to door, passing out flyers and bumper stickers, giving local presentations, and getting on local radio and TV. But in a national election, those efforts are easily trumped by the mass media. And local governments too are beholden to big money.

When governments of any size need to borrow money, the megabanks in a position to supply it can generally dictate the terms. Even in Greece, where the populist Syriza Party managed to prevail in January, the anti-austerity platform of the new government is being throttled by the moneylenders who have the government in a chokehold.

How did we lose our democracy? Were the Founding Fathers remiss in leaving something out of the Constitution? Or have we simply gotten too big to be governed by majority vote?

Democracy’s Rise and Fall

The stages of the capture of democracy by big money are traced in a paper called “The Collapse of Democratic Nation States” by theologian and environmentalist Dr. John Cobb. Going back several centuries, he points to the rise of private banking, which usurped the power to create money from governments:

The influence of money was greatly enhanced by the emergence of private banking. The banks are able to create money and so to lend amounts far in excess of their actual wealth. This control of money-creation . . . has given banks overwhelming control over human affairs. In the United States, Wall Street makes most of the truly important decisions that are directly attributed to Washington.

Today the vast majority of the money supply in Western countries is created by private bankers. That tradition goes back to the 17th century, when the privately-owned Bank of England, the mother of all central banks, negotiated the right to print England’s money after Parliament stripped that power from the Crown. When King William needed money to fight a war, he had to borrow. The government as borrower then became servant of the lender.

In America, however, the colonists defied the Bank of England and issued their own paper scrip; and they thrived. When King George forbade that practice, the colonists rebelled.

They won the Revolution but lost the power to create their own money supply, when they opted for gold rather than paper money as their official means of exchange. Gold was in limited supply and was controlled by the bankers, who surreptitiously expanded the money supply by issuing multiple banknotes against a limited supply of gold.

This was the system euphemistically called “fractional reserve” banking, meaning only a fraction of the gold necessary to back the banks’ privately-issued notes was actually held in their vaults. These notes were lent at interest, putting citizens and the government in debt to bankers who created the notes with a printing press. It was something the government could have done itself debt-free, and the American colonies had done with great success until England went to war to stop them.

President Abraham Lincoln revived the colonists’ paper money system when he issued the Treasury notes called “Greenbacks” that helped the Union win the Civil War. But Lincoln was assassinated, and the Greenback issues were discontinued.

In every presidential election between 1872 and 1896, there was a third national party running on a platform of financial reform. Typically organized under the auspices of labor or farmer organizations, these were parties of the people rather than the banks. They included the Populist Party, the Greenback and Greenback Labor Parties, the Labor Reform Party, the Antimonopolist Party, and the Union Labor Party. They advocated expanding the national currency to meet the needs of trade, reform of the banking system, and democratic control of the financial system.

The Populist movement of the 1890s represented the last serious challenge to the bankers’ monopoly over the right to create the nation’s money. According to monetary historian Murray Rothbard, politics after the turn of the century became a struggle between two competing banking giants, the Morgans and the Rockefellers. The parties sometimes changed hands, but the puppeteers pulling the strings were always one of these two big-money players.

In All the Presidents’ Bankers, Nomi Prins names six banking giants and associated banking families that have dominated politics for over a century. No popular third party candidates have a real chance of prevailing, because they have to compete with two entrenched parties funded by these massively powerful Wall Street banks.

Democracy Succumbs to Globalization

In an earlier era, notes Dr. Cobb, wealthy landowners were able to control democracies by restricting government participation to the propertied class. When those restrictions were removed, big money controlled elections by other means:

First, running for office became expensive, so that those who seek office require wealthy sponsors to whom they are then beholden. Second, the great majority of voters have little independent knowledge of those for whom they vote or of the issues to be dealt with. Their judgments are, accordingly, dependent on what they learn from the mass media. These media, in turn, are controlled by moneyed interests.

Control of the media and financial leverage over elected officials then enabled those other curbs on democracy we know today, including high barriers to ballot placement for third parties and their elimination from presidential debates, vote suppression, registration restrictions, identification laws, voter roll purges, gerrymandering, computer voting, and secrecy in government.

The final blow to democracy, says Dr. Cobb, was “globalization” – an expanding global market that overrides national interests:

[T]oday’s global economy is fully transnational. The money power is not much interested in boundaries between states and generally works to reduce their influence on markets and investments. . . . Thus transnational corporations inherently work to undermine nation states, whether they are democratic or not.

The most glaring example today is the secret twelve-country trade agreement called the Trans-Pacific Partnership. If it goes through, the TPP will dramatically expand the power of multinational corporations to use closed-door tribunals to challenge and supersede domestic laws, including environmental, labor, health and other protections.

Looking at Alternatives

Some critics ask whether our system of making decisions by a mass popular vote easily manipulated by the paid-for media is the most effective way of governing on behalf of the people. In an interesting Ted Talk, political scientist Eric Li makes a compelling case for the system of “meritocracy” that has been quite successful in China.

In America Beyond Capitalism, Prof. Gar Alperovitz argues that the US is simply too big to operate as a democracy at the national level. Excluding Canada and Australia, which have large empty landmasses, the United States is larger geographically than all the other advanced industrial countries of the OECD (Organization for Economic Cooperation and Development) combined. He proposes what he calls “The Pluralist Commonwealth”: a system anchored in the reconstruction of communities and the democratization of wealth. It involves plural forms of cooperative and common ownership beginning with decentralization and moving to higher levels of regional and national coordination when necessary. He is co-chair along with James Gustav Speth of an initiative called The Next System Project, which seeks to help open a far-ranging discussion of how to move beyond the failing traditional political-economic systems of both left and Right..

Dr. Alperovitz quotes Prof. Donald Livingston, who asked in 2002:

What value is there in continuing to prop up a union of this monstrous size? . . . [T]here are ample resources in the American federal tradition to justify states’ and local communities’ recalling, out of their own sovereignty, powers they have allowed the central government to usurp.

Taking Back Our Power

If governments are recalling their sovereign powers, they might start with the power to create money, which was usurped by private interests while the people were asleep at the wheel. State and local governments are not allowed to print their own currencies; but they can own banks, and all depository banks create money when they make loans, as the Bank of England recently acknowledged.

The federal government could take back the power to create the national money supply by issuing its own Treasury notes as Abraham Lincoln did. Alternatively, itcould issue some very large denomination coins as authorized in the Constitution; or it could nationalize the central bank and use quantitative easing to fund infrastructure, education, job creation, and social services, responding to the needs of the people rather than the banks.

The freedom to vote carries little weight without economic freedom – the freedom to work and to have food, shelter, education, medical care and a decent retirement. President Franklin Roosevelt maintained that we need an Economic Bill of Rights. If our elected representatives were not beholden to the private moneylenders, they might be able both to pass such a bill and to come up with the money to fund it.

Henry Ford said, “It is well enough that the people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

We are beginning to understand, and Occupy Wall Street looks like the beginning of the revolution.

We are beginning to understand that our money is created, not by the government, but by banks. Many authorities have confirmed this, including the Federal Reserve itself. The only money the government creates today are coins, which compose less than one ten-thousandth of the money supply. Federal Reserve Notes, or dollar bills, are issued by Federal Reserve Banks, all twelve of which are owned by the private banks in their district. Most of our money comes into circulation as bank loans, and it comes with an interest charge attached.

According to Margrit Kennedy, a German researcher who has studied this issue extensively, interest now composes 40% of the cost of everything we buy. We don’t see it on the sales slips, but interest is exacted at every stage of production. Suppliers need to take out loans to pay for labor and materials, before they have a product to sell.

For government projects, Kennedy found that the average cost of interest is 50%. If the government owned the banks, it could keep the interest and get these projects at half price. That means governments—state and federal—could double the number of projects they could afford, without costing the taxpayers a single penny more than we are paying now.

This opens up exciting possibilities. Federal and state governments could fund all sorts of things we think we can’t afford now, simply by owning their own banks. They could fund something Franklin D. Roosevelt and Martin Luther King dreamt of—an Economic Bill of Rights.

A Vision for Tomorrow

In his first inaugural address in 1933, Roosevelt criticized the sort of near-sighted Wall Street greed that precipitated the Great Depression. He said, “They only know the rules of a generation of self-seekers. They have no vision, and where there is no vision the people perish.”

Roosevelt’s own vision reached its sharpest focus in 1944, when he called for a Second Bill of Rights. He said:

This Republic had its beginning, and grew to its present strength, under the protection of certain inalienable political rights . . . . They were our rights to life and liberty.

As our nation has grown in size and stature, however—as our industrial economy expanded—these political rights proved inadequate to assure us equality in the pursuit of happiness.

He then enumerated the economic rights he thought needed to be added to the Bill of Rights. They included:

The right to a job;

The right to earn enough to pay for food and clothing;

The right of businessmen to be free of unfair competition and domination by monopolies;

The right to a decent home;

The right to adequate medical care and the opportunity to enjoy good health;

The right to adequate protection from the economic fears of old age, sickness, accident, and unemployment;

The right to a good education.

Times have changed since the first Bill of Rights was added to the Constitution in 1791. When the country was founded, people could stake out some land, build a house on it, farm it, and be self-sufficient. The Great Depression saw people turned out of their homes and living in the streets—a phenomenon we are seeing again today. Few people now own their own homes. Even if you have signed a mortgage, you will be in debt peonage to the bank for 30 years or so before you can claim the home as your own.

Health needs have changed too. In 1791, foods were natural and nutrient-rich, and outdoor exercise was built into the lifestyle. Degenerative diseases such as cancer and heart disease were rare. Today, health insurance for some people can cost as much as rent.

Then there are college loans, which collectively now exceed a trillion dollars, more even than credit card debt. Students are coming out of universities not just without jobs but carrying a debt of $20,000 or so on their backs. For medical students and other post-graduate students, it can be $100,000 or more. Again, that’s as much as a mortgage, with no house to show for it. The justification for incurring these debts was supposed to be that the students would get better jobs when they graduated, but now jobs are scarce.

After World War II, the G.I. Bill provided returning servicemen with free college tuition, as well as cheap home loans and business loans. It was called “the G.I. Bill of Rights.” Studies have shown that the G.I. Bill paid for itself seven times over and is one of the most lucrative investments the government ever made.

The government could do that again—without increasing taxes or the federal debt. It could do it by recovering the power to create money from Wall Street and the financial services industry, which now claim a whopping 40% of everything we buy.

An Updated Constitution for a New Millennium

Banks acquired the power to create money by default, when Congress declined to claim it at the Constitutional Convention in 1787. The Constitution says only that “Congress shall have the power to coin money [and] regulate the power thereof.” The Founders left out not just paper money but checkbook money, credit card money, money market funds, and other forms of exchange that make up the money supply today. All of them are created by private financial institutions, and they all come into the economy as loans with interest attached.

Governments—state and federal—could bypass the interest tab by setting up their own publicly-owned banks. Banking would become a public utility, a tool for promoting productivity and trade rather than for extracting wealth from the debtor class.

Congress could go further: it could reclaim the power to issue money from the banks and fund its budget directly. It could do this, in fact, without changing any laws. Congress is empowered to “coin money,” and the Constitution sets no limit on the face amount of the coins. Congress could issue a few one-trillion dollar coins, deposit them in an account, and start writing checks.

The Fed’s own figures show that the money supply has shrunk by $3 trillion since 2008. That sum could be spent into the economy without inflating prices. Three trillion dollars could go a long way toward providing the jobs and social services necessary to fulfill an Economic Bill of Rights. Guaranteeing employment to anyone willing and able to work would increase GDP, allowing the money supply to expand even further without inflating prices, since supply and demand would increase together.

Modernizing the Bill of Rights

As Bob Dylan said, “The times they are a’changin’.” Revolutionary times call for revolutionary solutions and an updated social contract. Apple and Microsoft update their programs every year. We are trying to fit a highly complex modern monetary scheme into a constitutional framework that is 200 years old.

After President Roosevelt died in 1945, his vision for an Economic Bill of Rights was kept alive by Martin Luther King. “True compassion,” King declared, “is more than flinging a coin to a beggar; it comes to see that an edifice which produces beggars needs restructuring.”

MLK too has now passed away, but his vision has been carried on by a variety of money reform groups. The government as “employer of last resort,” guaranteeing a living wage to anyone who wants to work, is a basic platform of Modern Monetary Theory (MMT). A student of MMT declares on his website that by “[e]nding the enormous unearned profits acquired by the means of the privatization of our sovereign currency. . . [i]t is possible to have truly full employment without causing inflation.”

What was sufficient for a simple agrarian economy does not provide an adequate framework for freedom and democracy today. We need an Economic Bill of Rights, and we need to end the privatization of the national currency. Only when the privilege of creating the national money supply is returned to the People, can we have a government that is truly of the people, by the people and for the people.

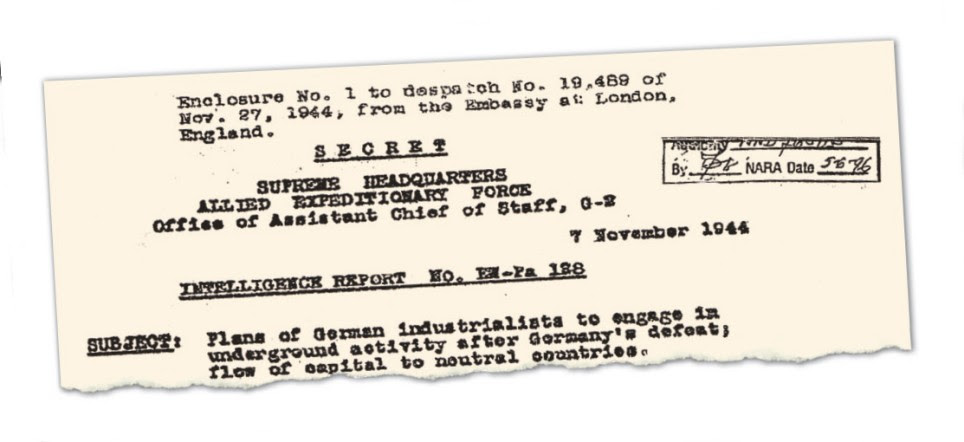

A few years ago, Newsweek and Guardian journalist Adam LeBor, who is known for his hard hitting journalism, was handed a secret World War II document called “Red House Report“. What was inside was incredible – written in 1944, EW-Pa 128, or as it’s more commonly known the “Red House Report” contained some shocking information.The three-page, closely typedreport, marked ‘Secret’, copied to British officialsand sent by air pouch to Cordell Hull, the US Secretary of State,detailed how the industrialists were to work with the Nazi Party to rebuild Germany’s economy by sending money through Switzerland. They would set up a network of secret front companies abroad. They would wait until conditions were right. And then nazis would take over Germany again. The industrialists included representatives of Volkswagen, Krupp and Messerschmitt. Officials from the Navy and Ministry of Armaments were also at the meeting and, with incredible foresight, they decided together that the Fourth German Reich, unlike its predecessor, would be an economic rather than a military empire – but not just German ….

Joseph Goebbels, Hitler’s propaganda minister, once said:

“In 50 years’ time nobody will think of nation states.”

Revealed: The secret report that shows how the Nazis planned

The arch architect of the strategic plan described in the “Red House Report”was no other than the SS Reichsführer Heinrich Himmler, according to this book :

When Christos Papaioannou noticed his car needed new tires, the Greek computer engineer bought them with euros—but used an alternative currency, called TEM, to pay his mechanic for the labor. His country has avoided a catastrophic exit from the common currency, at least for now. But a small but growing number of cash-strapped Greeks, who are still grappling with strict money-withdrawal limits, have found another route in TEM and other unconventional payment systems like it. Before then, Ms. Sotiropoulou said she was only aware of two such programs. No official record of the number of alternative currencies and local bartering systems appears to exist in Greece. But according to an Athens-based grass roots organization called Omikron Project, there are now more than 80 such programs, double the number in 2013. They vary in size, from dozens of members to thousands. – From the Wall Street Journal article: Alternative Currencies Flourish in Greece as Euros Are Harder to Come by

Hundreds of millions of people throughout the Western world are being forced to admit an obvious, yet uncomfortable reality. Democracy is dead. Your vote and your voice doesn’t matter. Not at all.

No group of people understand this as intimately as the Greeks. They voted for one thing, got something else, and in the process were unceremoniously reminded of their political irrelevance. The Greeks are now in a position to show the rest of us how it’s done. Communities need to take matters into their own hands and tackle challenges at the grassroots level. Nowhere is this more impactful and necessary than in the monetary realm, and some Greeks are already leading the charge.

When Christos Papaioannou noticed his car needed new tires, the Greek computer engineer bought them with euros—but used an alternative currency, called TEM, to pay his mechanic for the labor.

His country has avoided a catastrophic exit from the common currency, at least for now. But a small but growing number of cash-strapped Greeks, who are still grappling with strict money-withdrawal limits, have found another route in TEM and other unconventional payment systems like it.

“Money is sparse right now, but people still have the same skills and knowledge they had before the crisis,” said Mr. Papaioannou, part of a cooperative that founded TEM in the port city of Volos and one of nearly 1,000 registered users of the alternate currency there.

“Money is sparse right now, but people still have the same skills and knowledge they had before the crisis.”

Read that line over and over and over again until you realize how simple, elegant and accurate it is.

TEM—a sophisticated form of barter whose name is the Greek acronym for Local Alternative Unit—was founded in 2010 in the early months of Greece’s debt crisis with less than a dozen members. Now it includes dozens of participating local businesses that use the system to sell goods and services, including prepared food, haircuts, doctor visits, or even for renting an apartment.

It is a localized version of what Greece might have to turn to if a tentative bailout agreement reached this week is derailed, or ultimately fails. Before his resignation last month, former Finance Minister Yanis Varoufakis floated the idea of setting up a parallel-currency system based on IOUs in the event that Greece could no longer stay afloat using euros. Without a rescue, the idea of using IOUs is seen as the country’s most likely alternative.

Before then, Ms. Sotiropoulou said she was only aware of two such programs. No official record of the number of alternative currencies and local bartering systems appears to exist in Greece. But according to an Athens-based grass roots organization called Omikron Project, there are now more than 80 such programs, double the number in 2013. They vary in size, from dozens of members to thousands.

“The problems that existed have only gotten worse, and the new deal is going to create problems of its own that will deepen the crisis in certain areas,” said Mehran Khalili, one of the founders of Omikron. “The logical response is to create groups to react to that and fill those gaps that are going to exist because of the unsustainable situation that Greece has found itself in.

Experts say TEM and other local currencies work best side-by-side with the euro, not as a replacement.

“Experts” say. Yeah, the same so-called “experts” who destroyed the world economy and turned the planet into a thieving oligarchy. I think I’ve had enough “expert” economic advice for one lifetime.

One notable example of alternative currencies used during a crisis was in the 1930s during the Great Depression, when the Austrian town of Wörgl decided to fight the economic downturn by printing its own money. Economists called the result a miracle: Employment boomed, while inflation remained subdued. During the economic depression that struck Argentina in 1998 and lasted till 2002, people formed barter networks and several provinces introduced their own currencies.

The alternate currencies have their limitations: The use of TEM, for example is restricted to those people and local businesses that choose to accept them, and won’t directly help people struggling to meet their monthly utility bills.

Maria McCarthy, a British woman who lives in Volos with her Greek husband and children, has earned and spent over 10,000 TEMs in four years by offering English and guitar lessons. She also sells secondhand clothes and other material goods in Volos’ biweekly marketplace, where almost everything besides euros are exchanged.

Mr. Papaioannou says he has paid for renovating parts of his home as well as food and clothing with the currency, and an increasingly larger share of his computer-repair work is done through transactions with TEM.

“You’re used to a method of doing things,” he said, “and suddenly, you realize there are other ways too.”

You’ve gotta love the Greek spirit. You can knock them down, you can embarrass them, but you can’t kill their spirit. Everyone else on the planet must recognize that what is being done to Greece will be done to us all in turn. We must show totally solidarity with them against the euro-fascists.

“The currency developed by economist Silvio Gesell called “stamp scrip” [displayed above],almost saved Europe from fascism. It is explained in Bernard Lietaer’s magnificent book, The Future of Money. In its original form, stamp scrip was a piece of paper on which a number of boxes were printed. The note would lose its validity unless a stamp costing 1% of its value was stuck in one of the boxes every month. In other words, the currency lost value over time, so there was no incentive to hoard it. Stamp scrip projects took off across Germany and Austria after national currencies collapsed in the early 1930s. In 1932, for example, the town of Wörgl was almost broke, unable to finance public works or to support its destitute population, until the mayor heard of Gesell’s proposal. He put up the town’s tiny remaining fund as collateral against the same value of stamp scrip, and used it to pay for a building project. The workers then passed on the currency as quickly as they could. Like the magic pudding, this little pot of money kept circulating, enabling Wörgl to repave the streets, rebuild the water system, construct houses, a bridge and even a ski jump. In the 13 months of the experiment, the 5,500 scrip schillings in circulation were spent 416 times, creating between 12 and 14 times as much employment as the standard currency would have done. Unemployment vanished, and the stamp fees paid for a soup kitchen feeding 220 families. The governments of Germany and Austria, profoundly threatened by the success of these projects, shut them down and employment collapsed once more. When the US economist Irving Fisher examined these experiments he concluded that “the correct application of stamp scrip would solve the depression crisis in the US in three weeks!” Roosevelt’s government, aware that such currencies could invoke a massive loss of federal power, promptly banned it.”— George Monbiottheguardian.com

“The Argentine-German economist Silvio Gesell (1862-1930) wished to introduce “debt-free money.” Margrit Kennedy relates in her book Interest and Inflation Free Money (1988) how adherents to Gesell’s theory of a free economy in the 1930s made several attempts with interest-free currency in various countries, including Germany, Switzerland, Spain and the United States. Particularly successful was the model used in the small town of Woergl in the Tirol in Austria. In 1932 the ideas described in Gesell’s book Die natwerlicke Wirtschaftsordnung (The Natural Economic Order, 1916) were introduced. In August 1932 the town council of Woergl issued their own bank notes, called work certificates, to a value of 32,000 schillings. Backed by an equivalent amount of ordinary schillings in the bank, the town put 12,600 work certificates into circulation. The fee on the use of the money was 1 percent per month or 12 percent per year. This fee had to be paid by the person who had the banknote at the end of the month, in the form of a stamp worth 1 percent of the note glued to its back. The town paid for wages and building materials with this money. A ski-slope was built; streets were renewed as well as the canal system. They built bridges, improved roads and public services, and paid salaries and for materials with this money, which was accepted by the butcher, the shoemaker, the baker, by everyone. The small fee made everyone put this money into circulation before using one’s “real” money. Within a year 32,000 work certificates had been in circulation 463 times and thus had made possible the exchange of goods and services to value of 14,816,000 schillings. In comparison to the sluggish national currency it circulated eight times as fast. Unemployment was reduced by 25 percent within a year. When, however, 200 communities in Austria began to be interested in adopting this model the Austrian National Bank on September 1, 1933, prohibited the printing of any local currency. Unemployment returned, prosperity disappeared.”— Jüri Lina

“Wörgl’s demonstration was so successful that it was replicated, first in the neighboring city of Kirchbichl in January of 1933. In June of that year, Unterguggenberger addressed a meeting with representatives of 170 other towns and villages. Soon afterwards 200 townships in Austria wanted to copy it. It was at that point that the central bank panicked and decided to assert its monopoly rights. The people sued the central bank, but lost the case in November 1933. The case went to the Austrian Supreme Court, but was lost again. After that it became a criminal offence in Austria to issue “emergency currency.” … does it sound familiar? Only a central authority saviour can help people who are not allowed to help themselves locally.” — Bernard Lietaer, The Wörgl Experiment: Austria (1932-1933)

“For every local community currency dollar that was issued, we required the equivalent of a dollar’s worth of work done.”

” As of this summer, you can be broke in Santa Barbara, California, and still afford organic produce from the farmers’ market. You can be dollar-broke, that is—but if you have enough Santa Barbara Missions tokens jangling in your pocket, earned in exchange for helping out at a number of local nonprofits, you’ll be set. Santa Barbara Missions tokens, a new local currency in Santa Barbara, began circulating in July, soon after California Gov. Jerry Brown signed a law repealing a section of the state’s corporation code that prohibited the issuance of currencies other than the dollar : http://www.samabank.org/sb_missions/

The Santa Barbara County Local Community Currency are tokens created for the purpose of monetizing volunteer work of mission-driven organizations in the Santa Barbara community. Normally volunteerism is a privilege for people whose basic needs are already cared for. Our Local Community Currency level the socio-economic landscape by offering people means to meet their basic needs through their volunteer work.

The Santa Barbara Local Community Currency :

The Santa Barbara Local Community Currency facilitates creation of a unique parallel economy based on the premise that a service to our community can be a basis for our livelihood. Normally it is a privilege to volunteer for mission-driven organizations whose work inspires us. The SB Mission currency transform the norm by remunerating volunteers for their work with Local Community Currency, thereby enabling anyone to help meet their livelihood needs through service to the community. For example, people who struggle with access to good food can earn local currency working with the Food Co-Op, spend the earned Local Community Currency for produce and meals, while learning valuable life skills and participating in strengthening the food independence of their own community:

Local currencies are one way of ensuring life goes on in hard times.

Just 30 miles from Rosenheim, the birthplace of the chiemgauer, is the Austrian town of Wörgl. In 1932, during the Great Depression, Wörgl issued its own currency – it was so successful that it became known as “das Wunderwaffe von Wörgl”, impressing John Maynard Keynes.

The chiemgauer started as a school project by Christian Gelleri, an economics teacher in southern Germany who wanted to teach a group of 16-year-olds about finance in a novel way – by creating their own money, to be used in local shops and businesses. They called it the “chiemgauer” and eight years on, the project has turned into the world’s most successful alternative currency;it’s off the scale in comparison with others. The chiemgauer has managed to bring on board local co-operative banks and credit organisations, and it’s even possible to pay in chiemgauer using a debit card, run by Regios, an association of co-operative banks.

What makes the chiemgauer different to conventional currency is that it automatically loses value if you don’t spend it. Unlike traditional money that can be saved, the chiemgauer is only valid for three months – the idea being that it must be spent, thereby boosting the local economy. If the notes aren’t spent, they can be renewed by buying a stamp that costs 2% of the note’s face value – so over a year, the currency depreciates 8%. Notes can be renewed up to seven times. That might sound off-putting, but users are happy with the system. Angela Hamberger from the small town of Trostberg, explains how it works: “You can use the chiemgauer in all sorts of shops – from the hairdresser’s to the baker’s. You just have to register in the scheme and go to a participating bank to change your euro into chiemgauer. It’s worth it to support the community.” When registering, users nominate one of 230 local charities and organisations to receive 3% of their chiemgauer transactions. The chiemgauer, named after a region in Bavaria, is now accepted by more than 600 businesses in the Rosenheim-Traunstein area where it operates. It is estimated that around 2,500 people regularly use the currency and along the way it has also earned more than €100,000 for local non-profit organisations. Since its debut, 14 million euroshave been exchanged into the Chiemgauer.

Alternative currencies can play a vital role in that, which enable consumers and producers to exchange with each other across a larger area and based upon values other than globalisation.In a world obsessed with speculation, the chiemgauer has certainly got the Germans thinking again about what money is primarily for — paying people to deliver services and products and creating employment :

(DEBT) FREE MONEY! DIGITAL CURRENCIES ARE BRINGING MONEY BACK TO THE PEOPLE — WITHOUT INTEREST :

“After the end of the first World War, Germany began its national credit program by devising a plan of public works. Projects earmarked for funding included flood control, repair of public buildings and private residences, and construction of new buildings, roads, bridges, canals, and port facilities. The projected cost of the various programs was fixed at one billion units of the national currency. One billion no-interest (debt-free) bills of exchange, called Labor Treasury Certificates, were then issued against this cost. Millions of people were put to work on these projects, and German workers were paid with the Treasury Certificates. This government-issued money wasn’t backed by gold, but it was backed by something of real value. It was essentially a receipt for labor and materials delivered to the government — “For every mark that was issued, we required the equivalent of a mark’s worth of work done or goods produced.” The workers then spent the Certificates on other goods and services, creating more jobs for more people:

Within two years, the unemployment problem had been solved and Germany was back on its feet. It had a solid, stable currency, no debt, and no inflation, at a time when millions of people in the United States and other Western countries were still out of work and living on welfare.”

In 1815 Guernsey needed a new market hall. There was no money. Then somebody proposed that the island should avail itself of its ancient prerogative and issue its own interest-free money. At first the proposal was turned down, but as they urgently needed 5,000 pounds and only had 1,000 pounds in hand, the Bailiff Daniel de Lisle Brock in 1816 decided to issue 4,000 pounds in one-pound interest-free Guernsey state notes. This was in addition to the current supply of English pounds, which two main banks were circulating on the island already.

Work was begun on the market hall, everything being paid for with this new money. When the hall was finished, customers arrived, and business was better than expected. By 1822 the market hall was paid for. The 4,000 one-pound notes were destroyed. The first project with the new money was so successful that it was soon followed by others. Next a new road was needed; there was gravel, stone and plenty of labor—but no money to pay for it. In all, the states issued 55,000 pounds’ worth of notes, which paid for the rebuilding of the market. A new school was built, then several more, the whole surroundings of the market hall were renewed, and several other public buildings were constructed, as well as widening of the streets. A new harbor was built along with the best new roads in Europe and sewers. The sum was paid for with taxation, and the notes were again destroyed. All these projects provided employment and economic stimulation.

In 1827 de Lisle Brock was able to speak of “the improvements which are the admiration of visitors and which contribute so much to the joy, the health and well-being of the inhabitants.” Things had certainly improved since 1815. It is significant that the great depression never troubled Guernsey. There was no unemployment, and the income tax was 10 pence on the pound. Things got even better. The import of expensive English flour was reduced. The money supply never exceeded 60,000 pounds. Unemployment was practically nonexistent. Guernsey became a prosperous island community.

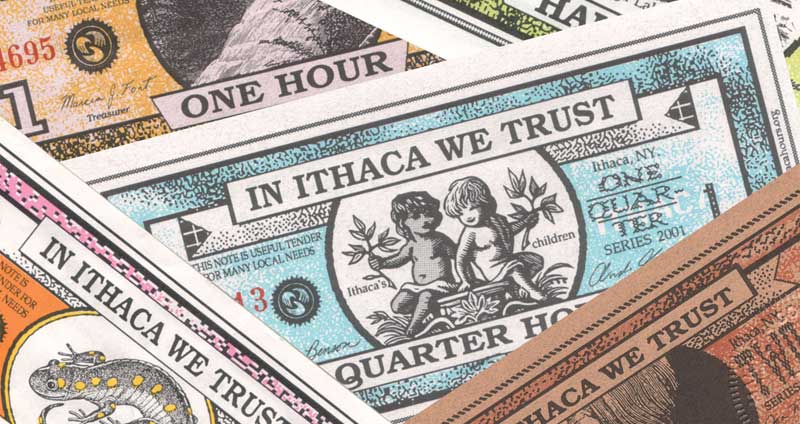

Scott Morris was born in Atlanta, GA, and raised in northern Alabama. While studying abroad in Japan during his studies at the University of Alabama, Scott took 5 weeks to backpack around China and SE Asia. It was there that he discovered his passion for helping the economically disempowered and made a commitment to bringing new pathways out of poverty to those who needed them most. He was featured in the powerful documentary “Money & Life” for his work with the volunteerism empowering “HERO Rewards” program he led the design and piloting of in Fairfield, Iowa. Now, he lives in Ithaca, NY, where he has founded the “AmeriQoin Cooperative” as a way for communities to benefit from world-class “community impact currency” technology without having to bear the full financial costs of developing and maintaining it.

AmeriQoin is a North American agency for community currencies. It provides designer currency systems and implementation assistance to existing currencies, grassroots organizations, and local networks for social, environmental, and commercial purposes. AmeriQoin provides currency system engineering expertise, consulting, and implementation assistance to existing community currencies, grassroots organizations, local business networks, and others seeking to create and deploy designer and/or targeted currency programs for social, environmental, and commercial purposes. AmeriQoin is to community currencies as BALLE is to “local first” organizations. CONTACT: support@ithacash.org

Scott Morris:“I will share my understanding of the true nature of money as a social construct and agreement that goes largely unexamined. I’ll also stress the importance of combating our econo-cultural myopia by bringing new metrics into the way we evaluate the success of the economy, and of our society on the whole. Finally, I’d like to make an argument and forecast that we’re on the verge of something truly revolutionary in the way we think about and interact with money. We could very well end up not only healing our relationships with one another and the Earth, but actually ushering in a new golden age for humanity.”

A startup local currency has just launched the Ithaca dollar in Ithaca, NY, designed to not only promote investment in local businesses and bring the community together, but to also pick up where one of the most successful alternative currency experiments in the US, the Ithaca HOURs, has left off.

The new Ithaca dollar is produced by a company called Ithacash, and for the moment is exclusively in digital form. The company founder, Scott Morris, is keen to keep local money within the local community. Local currencies “generate a lot of social and economic wealth,” said Morris to CNYcentral.

The new currency has a one to one parity with the US dollar, although when an individual buys into the scheme they receive 125 Ithaca dollars for their first $100 deposit. This equates to i$100 to spend in the community and i$25, which they can donate to a cause of their choosing “as a thank you for sacrificing the liquidity that you had with those US dollars,” explains Morris.

Over 100 local businesses have so far signed up to the scheme, with some already accepting payments via text message. Paper bills are also planned, although federal law prohibits the use of coins and denominations of a value less than a dollar.

Local sentiment towards the initiative is positive. Tyler Kenney, a student at Ithaca College, said:

“You have locals who are struggling against larger businesses and now you’re willing to help out the little guy, so I think it’s great.”

Another local resident Sarah Schmidlin added:

“It’s gonna support local businesses as opposed to people taking their money elsewhere.”

Ithaca HOURs

In 1991, another alternative currency called the Ithaca HOUR was introduced by a local businessman called Paul Glover. An Ithaca HOUR was valued at US$10 and was recommended as roughly equivalent to payment for one hour’s work. As such, they were produced in denominations of half, quarter and even an eighth of an Ithaca HOUR.

The scheme was a glowing success, with several million dollars worth of HOURs traded between residents and over 500 local businesses in the twenty years following its inception.

However, the shift towards electronic transactions over cash, combined with the founder of (and chief evangelist for) the currency moving out of town, led to a decline in its use. By 2011 few businesses were still accepting HOURs, and those that did couldn’t sustain a healthy flow.

The good news is that residents still holding Ithaca HOURs are being invited by Ithacash to convert them into Ithaca Dollars at a rate of i$17.50 for 1 HOUR (the equivalent of US$10 in 1991) “as a way of honoring that original commitment and to thank those still holding Ithaca HOURs for their continued loyalty to Ithaca’s economic well-being.”

B2B currencies aim to create additional revenue for Small and Medium Enterprises (SMEs), by providing businesses a complementary means of financing and payment. By facilitating SMEs to trade with each other using a B2B currency instead of Euro’s or Dollars, such instruments offer SMEs an improved liquidity position and a stronger business performance at the same time. Ultimately, B2B currencies help expand the size of the real economy and safeguard the health of local SMEs.

This type of currencies create added value in the local economy. Businesses using a B2B currency experience several benefits, including:

Reduce expenditures in Euro’s, Dollars and other currencies

Increase turnover and profitability

Gain availability of cheap and fast working capital at interest-free rates

Have access to new channels to commercialise own products and services

Which overall allow entrepreneurs to plan and look at the future with confidence.

B2B currencies operate alongside the Euro and other conventional currencies, and are able to reach multiple goals, among which:

Build a resilient local economy and strengthen SMEs

Drive up sales, liquidity and profits of participating businesses

Strengthen local supply chains and value networks

Research has demonstrated that such instruments are counter-cyclical with GDP, meaning they provide residual spending power during recessions, which has positive effects to combat unemployment in small businesses.

B2B currencies are technologically enabled solutions delivering meaningful economic impacts. Transactions are carried out seamlessly via various (electronic) means like web interfaces, mobile app, mobile texts (sms) and NFC technology.

The WIR Bank, formerly the Swiss Economic Circle (Wirtschaftsring-Genossenschaft), or WIR, is an independent complementary currency system in Switzerland that serves businesses in hospitality, construction, manufacturing, retail and professional services. WIR issues and manages a private currency, called the WIR Franc, which is used, in combination with Swiss Franc to generate dual-currency transactions. The WIR Franc is an electronic currency reflected in clients’ trade accounts and there is no paper money. The use of this currency results in increased sales, cash flow and profits for a qualified participant. WIR has perfected the system by creating a credit system which issues credit, in WIR Francs, to its members. The credit lines are secured by members pledging assets. This ensures that the currency is asset-backed. When two members enter into a transaction with both Swiss Francs and WIR Francs it reduces the amount of cash needed by the buyer; the seller does not discount its product or service. WIR was founded in 1934 by businessmen Werner Zimmermann and Paul Enz as a result of currency shortages and global financial instability. A banking license was granted in 1936. Both Zimmermann and Enz had been influenced by German libertarian economist Silvio Gesell; however, the WIR Bank renounced Gesell’s “free money” theory in 1952, opening the door to monetary interest. “WIR” is both an abbreviation of Wirtschaftsring and the word for “we” in German, reminding participants that the economic circle is also a community. According to the cooperative’s statutes, “Its purpose is to encourage participating members to put their buying power at each other’s disposal and keep it circulating within their ranks, thereby providing members with additional sales volume.” Although WIR started with only 16 members, today it has grown to include 62,000. Total assets are approximately 3.0 billion CHF, annual sales in the range of 6.5 billion, as of 2005. As of 1998, assets held by the credit system were 885 million and liabilities of 844 million, i.e. the circulating WIR money, with equity in the system of 44 million. These WIR obligations being interest free have a cost of zero. Income from interest and credit clearing activities were 38 million francs. The currency code is CHW as designated by ISO 4217. The WIR Bank was a not-for-profit entity, although that status changed during the Bank’s expansion. It has a stable history, not prone to failure as the current banking system is. It has remained fully operational during times of general economic crisis. The WIR Bank may even dampen downturns in the business cycle, helping to stabilize the Swiss economy during difficult times.

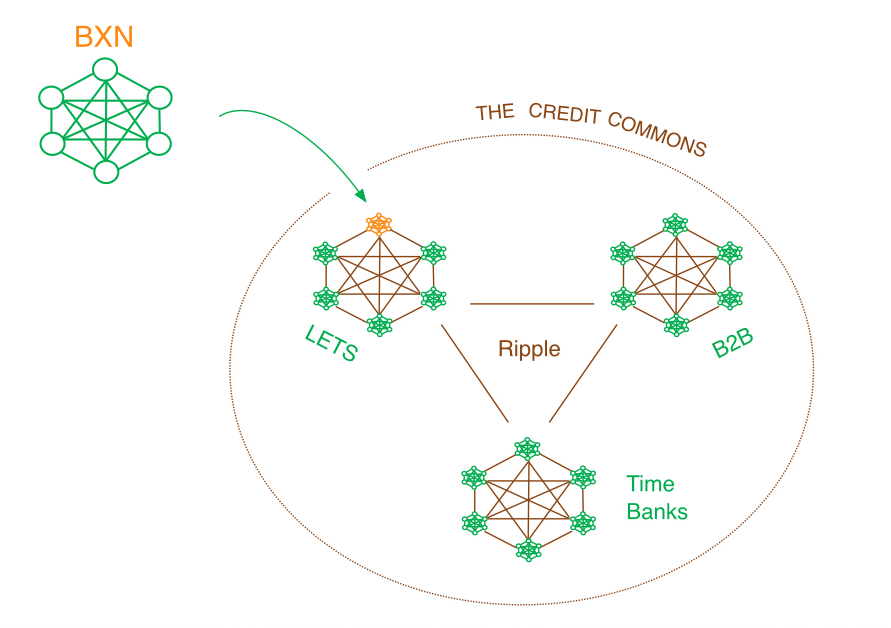

ZIGGY’s own LOCAL crypto-BANKING Revolution blue-print:

In short, initially I envision simultaneously creating two community currency systems in a single “local community.” When I say “local community,” I mean the size of it must be manageable by means of effective local grass-roots democracy.

This currency that I call CommonsQoin, by definition is not going to be privately owned, but it should belong to local community’s co-operative monetary organization, naturally belonging in the commons, sort of like free softwareUbuntuhttp://community.ubuntu.com/

First one will be a B2B currency — a mutual credit system modeled (with modifications) on the Swiss WIR Bank.

Second one (the so-called conventional counterpart) will be modeled (with modifications) on ithacash.org , and on the one in Bavaria, Germany.

Initially, they will function and grow separately. If everything develops well on both sides (as it should), and both sides come to economically sound agreement, there should be no problem to unite both currency systems, since it is essentially the same currency — CommonsQoin, but at the same time it is under strictly local control on either side. However, if in the future anything goes wrong on either side, they can decide to split and to function separately again.

A good hypothetical real life example would be uniting the Swiss WIR b2b currency with the Bavarian community currency, assuming they both were inthe same country.

Let’s assume that we achieve the same success in our “local community”, like in Bavaria, Germany. The next step would be to simply copy and paste that success to as many “local communities” across Canada and the US as possible.

The more “local communities” will adopt this ready out-of-the-box system, the greater the chance that two or more local communities will be in geographic proximity. If two adjacent “local communities” agree, they may enter into mutual acceptance of their local currencies, and in this way extend the territory of their “local community”, and the territory of mutual trade since it is essentially the same currency — CommonsQoin, but at the same time it is under strictly local control of the most “local community” unit. However, if in the future anything goes wrong they can decide to split and to function separately again, or even fold on either side.

By the same token, for instance, a local B2B currency system could, if desired, split with its conventionalcounterpart system in one local community and join another B2B, or conventional , or both, in adjacent local community. Full flexibility.

Because “local community” is a relative term (subject to definition) the best case scenario is that we could have Canada and the US as one big “local community” using one community currency — CommonsQoin. We could even think of it as an alternative bi-national currency.

The most important feature would be that there will be no Central Bank in charge of CommonsQoin system, as the democratic debt-free money creation power will reside with every single, most local community unit of the system.

Let’s globalize the LOCALIZATION.

This system is leader-less (centralbank-less), a peer-to-peer network model, so it can not be overtaken “from the top”, nor “assassinated” (from the top), nor infiltrated by rouge, trojan-horse communities (under hidden influence of private banksters), because any such local community can be easily disconnected from the rest of this democratic network, and sued for damages, if needed.

Needless to say, all the prior barter, time-share and community currency systems can, in principle, be easily converted and assimilated intoour local-globalCommonsQoin system, should they wish to join our grass-roots local democratic community global monetary revolution.

This is just the roughest outline, and there are many more strategic details of this system that have great potential for easily creating lots of local jobs.

Let’s create informal think-tank to fully develop this idea —the grass-roots, democratic, local-global “COMMUNITY CURRENCY System, version 2.0 “,code named:CommonsQoin ?

There seems to be a “weak link” in my CommonsQoin system, but I think I’ve just found a reasonable solution to it. The “weak link” is related to the fact that most often local communities do not geographically overlap with regional B2B networks.

It is not difficult to imagine that, for example, the Swiss b2b WIR currency system may not be enthusiastic about monetary union with other local community currency systems.

Therefore, we need something in-between to facilitate this strategically important monetary union. Such monetary “interface” should be a hybrid that is half “community”, and half“business” by its very nature. Good news is that we already have it — worker co-ops :

More precisely, in order for a community currency system to enter into monetary union with a B2B network, such community should start by developing new community worker co-ops that by definition must be bi-currency from the start, with emphasis on community currency, of course.

Obvious question is where do we get the money to invest in creation of such a newcommunity worker co-op? A part of the capital, in a form of the national currency, should ideally come from the community currency “bank” (credit union?) that naturally exchanges national currency for community currency.

The rest of the capital (human capital), could come from people in community contributing, in semi-volunteer fashion, their time, effort, and skills to getting this newcommunity worker co-op up and running in exchange for credit denominated in community currency. The emphasis in “semi-volunteer” is on “volunteer”, because community build this for long-term future community’s economic benefit, and everyone who contributes to the start of this new local democratic economy will be honestly compensated, even if they have to wait a bit to be paid.

Once a community worker co-op is ready to do business, initially, interested people could work for only 2 hours a day, quarter-time, and not even everyday, as there are more and more unemployed and under-employed people, and be paid in community currency for their semi-volunteer effort — democratic community currency money creation power: “For every local community currency dollar that was issued, we required the equivalent of a dollar’s worth of work done.”

Later, at the point when a community worker co-op is going steady and full-steam, mostly full-time jobs would be created, that could be paid in community currency that could be partially exchanged into national currency, if needed.

Let’s imagine that our community has a worker co-op in a form of a chain of Supermarket stores for locally produced foods and goods from the related regional B2B network.

And let’s imagine that our community also has an Affordable Housing worker co-op. So, for example, a worker from a community Supermarket co-op could pay rent to community housing co-op in community currency.

Please, excuse me that all of this is very sketchy, therefore I do need you to fill in the important tactical and technical details.

What are Economists Saying About Iceland’s Sovereign Money Proposal?

A study recently commissioned by the Icelandic prime minister, Sigmundur Gunnlaugsson, and written by Frosti Sigurjonsson, displays an accurate analysis of how banks create money and endorses Sovereign Money proposals. But what are people saying about the report? Of course there are criticisms of the report and some of the usual misunderstandings, but most people think it’s a proposal that merits serious consideration.

“The key idea is a new Sovereign Monetary System, where only the central bank is responsible for money creation. The idea makes sense…Separating the creation of money and allocation of money powers could safeguard against excessive credit creation, and reduce incentives for commercial banks to create more credit to make private gains…Iceland’s proposal is worth exploring.”

“It proposes a radical structural solution to the problems we face. The feasibility and merits of that specific solution need to be debated. But whatever the precise policies pursued, they must be grounded in the philosophy which this report proposes – that money creation is too important to be left to bankers alone.”

“Having decided against scrapping its currency, the government in Reykjavik now mulls a complete ban on its banks creating krona when they issue new loans…In recent years Scandinavian central bankers have shown the same dauntless appetite for exploration that once saw Nordic ships fan out across the globe. In this spirit Reykjavik should give sovereign money a shot. Nations far bigger and meaner than Iceland have struggled to come to grips with financial excess through conventional means. As well as showing other countries a potential way forward, by bringing the axe down on fractional reserve banking the Icelanders might just regain some control over their economic destiny.”